Dennis Matthews Scrutinises the Finkel Energy Report

“The report recommends a Clean Energy Target as the mechanism for the electricity sector.”

The trouble with recommending ‘clean’ as distinct from ‘renewable’ is that ’clean’ means ‘low greenhouse gas emissions’, and hence opens up the electricity sector to nuclear power, which is definitely not environmentally clean in the more general sense and nuclear advocates will attempt to argue that, from an Australian viewpoint, nuclear power is ‘low emission’.

![]() Dennis Matthews June 2017 Comments on“Independent Review into the Future Energy Security of the National Electricity Market Blueprint for the Future Alan Finkel June 2017”

Dennis Matthews June 2017 Comments on“Independent Review into the Future Energy Security of the National Electricity Market Blueprint for the Future Alan Finkel June 2017”

INTRODUCTION

The Finkel report recommendations involve greater regulation of an already highly regulated electricity market. These regulations are due to serious market failure, especially in those states that have privatised the electricity industry, yet nowhere is the possibility of de-privatisation (re-nationalisation) considered. The report’s answer to market failure is more, and more complicated, regulation and government funding. For example:

- the Australian Energy Market Operator (AEMO) “should develop a list of potential priority projects, in each region, that governments could support if the market is unable to deliver the investment required”.

- For the priority projects, the Australian Energy Market Commission (AEMC) should give guidance for governments on the circumstances “that would warrant government intervention to facilitate specific transmission investments.”

- “The Australian Competition and Consumer Commission should make recommendations on improving the transparency and clarity of electricity retail prices”.

The Finkel report, and its recommendations, contain many references to frequency control and fast frequency response but there are only two brief mentions in the report of direct current (DC) electricity, for which frequency control and fast frequency response are irrelevant.

The way in which the report refers to the financial year is ambiguous, for example:

“AEMO forecasts a potential supply shortfall in Victoria and South Australia for the FY2018 summer.”

This statement could refer to either the 2017-18 summer (end of 2107 to beginning of 2018) or to the 2018-2019 summer (end of 2018 to beginning of 2019).

The list of acronyms is far from complete which, particularly for domestic consumers, significantly hinders understanding the report.

The practice of compressing graphs (e.g., figures 3.5 to 3.7, and 3.9), making it difficult to determine trends and differences between various options, is unscientific. The scale of a graph should go from just below the lowest data point to just above the highest data point.

The following uses the same headings as in the report.

PREFACE

“There are no prohibitions, just incentives.”

‘Incentivisation’ is a word that is used frequently in the Finkel report. Mostly it means government subsidies. Not only are there no prohibitions but there are no penalties. There are no sticks just carrots. It is as if the privatised electricity industry, especially in South Australia, has not treated the consumer with contempt. ‘All is forgiven’, from now on we will start with a clean slate and trust the privatised electricity industry to do the right thing by the consumer.

The plan “ensures reliability by financially rewarding consumers for participating in demand response and distributed energy and storage.”

Well, actually not all consumers. Those, who by their profligate use of electricity have produced very high demand for electricity from the grid and helped push up spot wholesale prices by factors of up to 100, will get paid handsomely to turn off their air conditioners and pool pumps and thus will be able to buy even bigger air conditioners and get even greater payments the following year.

This particular carrot rewards the profligate consumer, it is an inefficiency incentive. What is needed is a big stick, one which clearly says, if you waste electricity you will get a much, much bigger electricity bill. We need to ‘incentivise’ electricity conservation, we need more efficiency incentives.

According to the Finkel report, if the blueprint is adopted by the government “then our National Electricity Market should return to being the high performance servant of our community that it once was.”

In the state, South Australia, which was the lead agency (legislator) for setting up the National Electricity Market (NEM) and which quickly privatised the electricity industry (despite an election promise to the contrary), domestic electricity prices have inexorably gone from bad to worse. The NEM plus privatisation has treated the SA community with contempt.

EXECUTIVE SUMMARY

“The report recommends a Clean Energy Target as the mechanism for the electricity sector.”

The trouble with recommending ‘clean’ as distinct from ‘renewable’ is that ’clean’ means ‘low greenhouse gas emissions’, and hence opens up the electricity sector to nuclear power, which is definitely not environmentally clean in the more general sense and nuclear advocates will attempt to argue that, from an Australian viewpoint, nuclear power is ‘low emission’.

On the question of gas supply:

“Governments should also work with communities to encourage safe exploration and production based on best available evidence, performance data and appropriate financial rights for landholder.”

There is mention of the rights of the traditional owners, or impact on water supply, or environmental issues.

Chapter 1

PREPARING FOR NEXT SUMMER

1.1 Improving the resilience of the NEM

The storms that hit SA in September 2016 are said to have “caused significant damage to key infrastructure”. It is no secret that the ‘key infrastructure’ was the high voltage alternating current (AC) transmission towers and lines.

Chapter 2

INCREASED SECURITY

Much of this chapter deals with problems of maintaining the frequency of the AC electricity network. One of the available technical solutions mentioned is direct current (DC) interconnectors but this solution is not pursued by the report. Instead, the focus is on synchronous (AC) generators and the modification of non-synchronous (DC) generators to help maintain system inertia and frequency.

“The Panel strongly supports a requirement for new generators (to) be able to provide FFR (Fast Frequency Response) services.”

This requirement is aimed at DC generators such as wind turbines and rooftop solar photovoltaic (PV) systems.

Rather than modify DC generators in order to support problematic AC systems, consideration should be given to enhancing and expanding the role of DC generators and networks.

Chapter 3

A RELIABLE AND LOW EMISSIONS FUTURE

3.2 A challenging and changing market environment

The report appears reticent to call a spade a spade, and to prefer what appears to be diplomatic code. For example,

“The difference in dispatch and settlement periods opens the possibility for strategic bidding behaviour”.

It seems that what the report means by ‘strategic bidding behaviour’ is what is commonly known as ‘gaming’, such as fossil fuel generators with-holding supply in order to force up the price, sometimes by factors of 100 or more.

This shyness in naming names is not evident when talking about ‘variable’ renewable energy electricity generators (VRE) such as wind and solar photovoltaics. For example,

“VRE generators are increasing price volatility in the wholesale market and are creating challenging investment conditions for other generators.”

It is noticeable that no non-renewable electricity generators (usually referred in the report as ‘synchronous’ generators) are referred to as ‘variable’ yet readily available data shows that some non-renewable generators only generate for a few days a year and others for only 10 or 20% of the year.

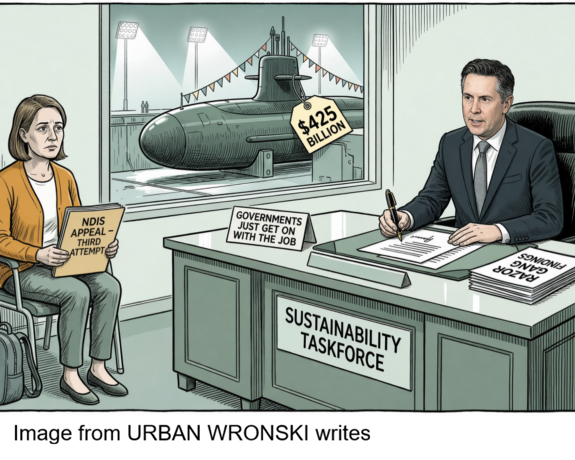

Despite many indications that the NEM is dysfunctional, at no stage does the report blame ‘the market’. Rather it prefers to continually point the finger at VRE generators. For the last 15 years, privatised electricity markets have been steadily aggregating into ‘gentailers’ – fossil fuel electricity generators acquiring retail assets and vice-versa – and concentrating market power into the hands of a few companies to the stage where three gentailers (Energy Australia, Origin and AGL) “now account for 64 per cent of generation capacity”. This oligopoly makes a mockery of free market economics.

Only after remedying major market distortions such as ‘vertical integration’ will it be possible to diagnose the system and to remedy any residual problems. It may well be that the problem resides in the privatisation of an essential service, including two natural monopolies (distribution and transmission), and that the only acceptable integrated electricity industry is one that is publicly owned and answerable to the consumer through 3-4 yearly elections. Needless to say, the report doesn’t even mention, let alone discuss, such a possibility.

Chapter 5

IMPROVED SYSTEM PLANNING

5.5 Dealing with the financial risk of stranded assets

The report draws attention to a serious failure of the NEM – the recent overinvestment in electricity networks (‘goldplating’), which resulted in higher profits for network owners and higher electricity prices for consumers and which, because of greater reliance on distributed renewable electricity generation and use, risks being underutilised (‘stranded’) – but decides to leave the problem to someone else:

“The issue of the historic network over-investment is beyond the scope of this Review, and it is not possible to examine this issue in detail”.

Chapter 6

REWARDING CONSUMERS

This report is more about rewarding network owners than about rewarding consumers. For example, the report notes the value of energy efficiency, such as building homes with better energy efficiency, in reducing peak demand

“In the long term, improvements in energy efficiency reduce electricity demand and generation capacity, reducing costs for (all) consumers.”

but concentrates on how consumers with rooftop solar electricity generators can stabilise the electricity network, thereby producing more business and profits for network owners.

Increasing energy efficiency of buildings, which competes with electricity generation, comes at a cost. But, unlike centralised electricity generation, the cost of making buildings energy efficient is met up-front by the consumer.

“Low-income or vulnerable consumers are unlikely to invest in energy efficiency and demand management due to the high upfront costs and imprecise benefits.”

Instead of addressing the upfront cost barrier to competition, the report chooses to put the burden on owners of distributed electricity. To protect low-income and vulnerable consumers the report suggests that we

“make sure that the distributed resources owned by other consumers are being used in a way that provides benefits not only to the owner but also to the whole electricity system.”

It would be interesting if this same philosophy were applied to centralised electricity generation resources.

The playing field is biased in favour of centralised electricity generation and against electricity savings through distributed energy efficiency. Upfront costs are a major deterrent to many labour intensive, small scale, distributed projects which, as shown by the rapidly escalating contribution from rooftop solar electricity, can make significant contributions both to employment and to electricity supply and demand.

By removing the upfront costs then everyone will be able to have access to distributed energy efficiency and supply in competition with large scale centralised electricity supply. This will reduce the number of “consumers who are not able to invest in their own alternatives to grid supplied electricity or energy efficiency” and to fewer disconnections through late payment of electricity bills.

Rooftop solar+battery installers are now starting to take this ‘no-upfront cost’ approach by, for example, renting roof space.

In addition to putting electricity efficiency on a competitive footing with electricity supply, reducing electricity demand can be assisted by making meter access more user- friendly. At the moment, most meters and their location are retailer-friendly but user-unfriendly. Making the meters more ‘computer-friendly’ is not likely to change this.

A user-friendly meter should be easily accessible in a convenient and prominent spot within a building, e.g., the kitchen or laundry, they should show real time power consumption both in kilowatts (e.g., a simple analogue meter, such as the speedometer or rpm meter in a car, calibrated 0-2-4-6-8kW) and $/day (for both peak and off-peak loads), and the progressive quarterly cost in $. Those who have rooftop solar generators will need additional information, especially that which gives real time information on how well the generator is performing.

6.4 Rewarding consumers for improving reliability and security

Demand response schemes involving consumers temporarily changing their usage of electricity at times of peak demand sounds like a good idea but in practice they are incentives to waste electricity. In the proposed schemes, consumers are rewarded (paid) to turn off their air conditioners and pool pumps. These rewards would go mostly to profligate electricity consumers; the more electricity being consumed the more that can be turned off and the more the consumer will be paid.

Distributed energy resources (DER) and demand response are seen as a resource for system security services such as improving power quality, and reducing voltage and frequency fluctuations. In doing this, they would also increase the use of an under-utilised electricity network and increase income for the network owners.

Such a role for DER would require coordinating small resources located at a large number of consumer’s houses as well as the electricity industry (generation, transmission, distribution and retail). According to the report, this could be done using an ‘aggregator’ company that coordinates the output of consumers. The aggregator would be the intermediary between the consumer-generator and the electricity industry.

Alternatively, the report gives the options of the DER being owned by the retailer, the transmission network owner, or the distribution network owner. This would lead to greater concentration of market power in an already overly concentrated electricity industry.

6.6 Improved energy efficiency

This a very short sub-section of the report. It’s one and only recommendation is:

“Recommendation 6.10

Governments should accelerate the roll out of broader energy efficiency measures to complement the reforms recommended in this review.”

This rather sterile, decades old, recommendation does nothing to remove the biggest hurdle to energy efficiency competing with centralised electricity generation, the upfront costs of energy efficiency measures, especially in the building industry.

Chapter 8

BEYOND THE BLUEPRINT

This chapter explores “some high potential technologies and projects that could be considered by governments and investors, which are beyond the scope of the blueprint, but may have a place in a future NEM.”

It will come as no surprise that this includes nuclear power, especially small modular reactors (SMRs).

8.3 Energy storage technologies

This section has a significant omission in that ‘Figure 8.1 Energy storage technologies’ does not include high temperature thermal storage which is a key component of solar thermal electricity generation, which however is covered in the section on ‘Concentrated solar thermal power and storage’. This technology is in a much more advanced stage of development than, say, small modular reactors and is being seriously considered for use in South Australia.

8.4 Electric vehicles

Electric vehicles are a highly advanced technology and, like rooftop photovoltaic electricity generation and battery storage, could easily go from being a minor player to a significant component of the electricity supply/demand equation in a decade. To relegate electric vehicles to ‘beyond the scope of the blueprint’ is to invite a repetition of the precarious situation in which the NEM is now embroiled and which is a key driver behind the need for the report.

No comments yet.

1 This month.

Australians deserve the truth

about

AUKUS – https://aukuspublicinquiry.com/

30 July – WEBINAR (Free) – Is Nuclear Power the Solution to Climate Change? https://my.acaw.org.au/event/acaw-is-nuclear-power-the-solution-to-climate-change

18:30 – 19:45 ACST

19:00 – 20:15 AEST

PETITION – To: Prime Minister Anthony Albanese and the Australian Labor Government

of the week – Australians for War Powers Reform (AWPR)

To see nuclear-related stories in greater depth and intensity

Leave a comment