Decommissioning, nuclear waste disposal – Holtec really has no incentive to make this safe for the long term

Nuclear Moral Hazard, Recent sales of U.S. nuclear plants raise

Nuclear Moral Hazard, Recent sales of U.S. nuclear plants raise  questions about safety, liability, and economic incentives. (Today’s post is co-authored with Catherine Hausman, an assistant professor at the University of Michigan.): Davis, Lucas and Catherine Hausman. “Nuclear Moral Hazard”, Energy Institute Blog, UC Berkeley, June 24, 2019,Last week, a company called Holtec International received federal approval to acquire New Jersey’s Oyster Creek nuclear power plant. Except Oyster Creek shut down last fall and will never produce another kilowatt-hour. Holtec is buying it to tear it down. It will be responsible for decommissioning the site, including managing spent fuel and other radioactive waste.

questions about safety, liability, and economic incentives. (Today’s post is co-authored with Catherine Hausman, an assistant professor at the University of Michigan.): Davis, Lucas and Catherine Hausman. “Nuclear Moral Hazard”, Energy Institute Blog, UC Berkeley, June 24, 2019,Last week, a company called Holtec International received federal approval to acquire New Jersey’s Oyster Creek nuclear power plant. Except Oyster Creek shut down last fall and will never produce another kilowatt-hour. Holtec is buying it to tear it down. It will be responsible for decommissioning the site, including managing spent fuel and other radioactive waste.

The Oyster Creek sale is one of several such recent transactions in which a U.S. nuclear plant is being sold by a large publicly-traded company to a smaller privately-owned company specializing in decommissioning. Though the other sales are pending approval by the Nuclear Regulatory Commission, it is not too soon to consider the potential implications for safety and the environment.

The U.S. nuclear industry has a strong record of safe operations. Historically, most owners of U.S. nuclear plants have been large companies, with significant “skin in the game” in terms of profitability and reputation if something were to go wrong. Do smaller companies have the same incentives? ………

Old Regime – Incentive for Safety

But, these nuclear asset transfers could have a big downside. In the past, safe operations meant that nuclear plants could make more money. We suspect that these economic incentives partly account for the good safety record of U.S. nuclear plants. Nuclear power plant owners worked hard to avoid problems because plant shutdowns are costly for plant owners.

Take Entergy, for example. At its peak, Entergy owned eight U.S. nuclear power plants, over 9,000 megawatts of nuclear capacity. With a large portfolio on the line, Entergy had an enormous incentive to make sure all its plants kept running without incident.

In short, under the old regime, it was profitable for nuclear operators to be extremely safe.

New Regime – Less to Lose

But that argument applied in an era when plants were actually generating electricity. Once plants close, this mechanism is no longer relevant – there are no operating profits on the line. Now the way to maximize profits is to minimize costs; so companies specializing in decommissioning will be working hard to figure out how to perform these functions as cheaply as possible.

And the reputation-based incentives also change. Before, companies worried that any problem at any plant would risk their reputation and thus their whole business – including other plants they owned and possibly including non-nuclear assets. But what about the new owners? Smaller companies have less to lose.

Bankruptcy protection is also an issue. For a company like Entergy with a $19 billion dollar market capitalization, only a large incident would put it out of business. Not true for a smaller company. Economists have long argued that bankruptcy protection raises a moral hazard problem – with “judgment proof” companies having less incentive to act safely.

Following in the Footsteps of Oil and Gas?

A similar moral hazard problem arises with oil and gas wells. Our colleague Judd Boomhower has writtenabout how small oil and gas producers face adverse incentives for safety and environmental risk. If the small oil and gas producer declares bankruptcy, it is not responsible for accident clean-up costs. Judd’s research shows that this can lead to less safe operating practices. Relatedly, the American West has thousands of “abandoned” wells that have not been properly remediated, many “owned” by companies that have gone bankrupt. Similar problems have shown up also with coal mines and offshore oil infrastructure. And the stakes for the nuclear sites are tremendous – across the country, we’re talking billions of dollars in anticipated clean-up costs.

Big Role for Regulation

When economic incentives alone do not ensure safe and thorough decommissioning, regulation should play a larger role. The new owners of these plants are inheriting substantial decommissioning funds, and the Nuclear Regulatory Commission has stated that it will be monitoring financial viability closely throughout the decommissioning process. But what happens if the new owners run out of money? Where will the necessary funds come from if the decommissioning funds prove insufficient to cover costs?

This is new territory for the Nuclear Regulatory Commission. As the U.S. nuclear generation fleet heads toward retirement, the NRC needs to pivot away from regulating construction and operation, and toward regulating decommissioning and fuel storage. Given the incentive issues these sales raise, it is critical that the NRC get up to speed quickly on the emerging risks.

Decommissionings at several recently-closed plants are aiming for accelerated timelines, which could be good or bad for safety. Between that and the specialized expertise that the new owners are bringing, the sales could turn out to be a win for the public. But the economic incentives for proper decommissioning are not very reassuring, and it’s not clear that regulations are ready to fill that gap. https://energyathaas.wordpress.com/2019/06/24/nuclear-moral-hazard/

No comments yet.

1 This month.

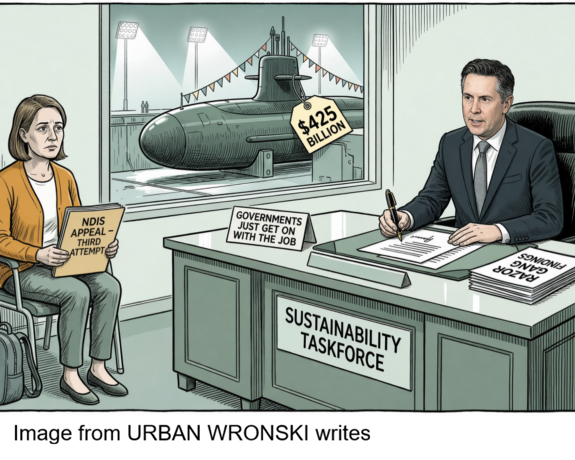

Australians deserve the truth

about

AUKUS – https://aukuspublicinquiry.com/

Australians deserve the truth

about AUKUS

PETITION – To: Prime Minister Anthony Albanese and the Australian Labor Government

of the week – Australians for War Powers Reform (AWPR)

To see nuclear-related stories in greater depth and intensity

Leave a comment