Why Nuclear Power Is Bad for Your Wallet and the Climate

Fashionably rebranded “Small Modular” or “Advanced” reactors can’t change the outcome. Their smaller units cost less but output falls even more, so SMRs save money only in the sense in which a smaller helping of foie gras helps you lose weight.

They’ll initially at least double existing reactors’ cost per kWh; that cost is ~3–13x renewables’ (let alone efficiency’s); and renewables’ costs will halve again before SMRs can scale. Do the math: 2 x (3 to 13) x 2 = 12–52-fold. Mass production can’t bridge that huge cost gap—nor could SMRs scale before renewables have decarbonized the US grid.

Even free reactors couldn’t compete: their non-nuclear parts cost too much. Small Modular Renewables are decades ahead in exploiting mass-production economies; nuclear can never catch up. It’s not just too little, too late: nuclear hogs market space, jams grid capacity, and diverts investments that more-climate-effective carbon-free competitors then can’t contest.

Why Nuclear Power Is Bad for Your Wallet and the Climate, https://news.bloomberglaw.com/environment-and-energy/why-nuclear-power-is-bad-for-your-wallet-and-the-climate, 17 Dec 21, Amory B. Lovins, Stanford University

As Congress and the Department of Energy pile new subsidies on nuclear power and the Nuclear Regulatory Commission seeks to gut its regulation, its marginal output additions have shrunk below 0.5% of the world market, says physicist Amory B. Lovins, adjunct professor of civil and environmental engineering at Stanford University. He explains why nuclear energy is not the answer to climate change, but actually worsens it due to climate opportunity cost.

Does climate protection need more nuclear power? No—just the opposite. Saving the most carbon per dollar and per year requires not just generators that burn no fossil fuel, but also those deployable with the least cost and time. Those aren’t nuclear.

Making 10% of world and 20% of U.S. commercial electricity, nuclear power is historically significant but now stagnant. In 2020, its global capacity additions minus retirements totaled only 0.4 GW (billion watts). Renewables in contrast added 278.3 GW—782x more capacity—able to produce about 232x more annual electricity (based on U.S. 2020 performance by technology). Renewables swelled supply and displaced carbon as much every 38 hours as nuclear did all year. As of early December, 2021’s score looks like nuclear –3 GW, renewables +290 GW. Game over.

The world already invests annually $0.3 trillion each, mostly voluntary private capital, in energy efficiency and renewables, but about $0.015–0.03 trillion, or 20–40x less, in nuclear—mostly conscripted, because investors got burned. Of 259 US power reactors ordered (1955–2016), only 112 got built and 93 remain operable; by mid-2017, just 28 stayed competitive and suffered no year-plus outage. In the oil business, that’s called an 89% dry-hole risk.

Renewables provided all global electricity growth in 2020. Nuclear power struggles to sustain its miniscule marginal share as its vendors, culture, and prospects shrivel. World reactors average 31 years old, in the U.S., 41. Within a few years, old and uneconomic reactors’ retirements will consistently eclipse additions, tipping output into permanent decline. World nuclear capacity already fell in five of the past 12 years for a 2% net drop. Performance has become erratic: the average French reactor in 2020 produced nothing one-third of the time.

China accounts for most current and projected nuclear growth. Yet China’s 2020 renewable investments about matched its cumulative 2008–20 nuclear investments. Together, in 2020 in China, sun and wind generated twice nuclear’s output, adding 60x more capacity and 6x more output at 2–3 times lower forward cost per kWh. Sun and wind are now the cheapest bulk power source for over 91% of world electricity

Nuclear Power Has No Business Case

Nuclear power has bleak prospects because it has no business case. New plants cost 3–8x or 5–13x more per kWh than unsubsidized new solar or windpower, so new nuclear power produces 3–13x fewer kWh per dollar and therefore displaces 3–13x less carbon per dollar than new renewables. Thus buying nuclear makes climate change worse. End-use efficiency is even cheaper than renewables, hence even more climate-effective. Arithmetic is not an opinion.

Unsubsidized efficiency or renewables even beat most existing reactors’ operating cost, so a dozen have closed over the past decade. Congress is trying to rescue the others with a $6 billion lifeline and durable, generous new operating subsidies to replace or augment state largesse—adding to existing federal subsidies that rival or exceed nuclear construction costs.

But no business case means no climate case. Propping up obsolete assets so they don’t exit the market blocks more climate-effective replacements—efficiency and renewables that save even more carbon per dollar. Supporters of new subsidies for the sake of the climate just got played.

Fashionably rebranded “Small Modular” or “Advanced” reactors can’t change the outcome. Their smaller units cost less but output falls even more, so SMRs save money only in the sense in which a smaller helping of foie gras helps you lose weight.

They’ll initially at least double existing reactors’ cost per kWh; that cost is ~3–13x renewables’ (let alone efficiency’s); and renewables’ costs will halve again before SMRs can scale. Do the math: 2 x (3 to 13) x 2 = 12–52-fold. Mass production can’t bridge that huge cost gap—nor could SMRs scale before renewables have decarbonized the US grid.

Even free reactors couldn’t compete: their non-nuclear parts cost too much. Small Modular Renewables are decades ahead in exploiting mass-production economies; nuclear can never catch up. It’s not just too little, too late: nuclear hogs market space, jams grid capacity, and diverts investments that more-climate-effective carbon-free competitors then can’t contest.

Meanwhile, SMRs’ novel safety and proliferation issues threaten threadbare schedules and budgets, so promoters are attacking bedrock safety regulations. NRC’s proposed Part 53 would perfect long-evolving regulatory capture—shifting its expert staff’s end-to-end process from specific prescriptive standards, rigorous quality control, and verified technical performance to unsupported claims, proprietary data, and political appointees’ subjective risk estimates.

But that final abdication can’t rescue nuclear power, which stumbles even in countries with impotent regulators and suppressed public participation. In the end, physics and human fallibility win. History teaches that lax regulation ultimately causes confidence-shattering mishaps, so gutting safety rules is simply a deferred-assisted-suicide pact.

Modern renewable generation keeps rising faster than nuclear output ever did in its 1980s heyday. During 2010–20, renewables reduced global power-sector carbon emissions 6x more than coal-to-gas switching (ignoring methane escape), and 5x more than nuclear growth.

Among compelling examples, Germany replaced both nuclear and coal generation with efficiency and renewables: in 2010–20, generation from lignite fell 37%, hard coal 64%, oil 52%, and nuclear 54%; gas power rose 3%; GDP rose 11% (17% pre-pandemic); power-sector CO2 fell 41%, meeting its target a year early with five percentage points to spare.

Japan’s savings and renewables meanwhile displaced 109% of lost nuclear output if adjusted for GDP growth, 95% if not, so its 21 “operational” reactors, shut for 10–14 years and counting, lost their market. And no country retains an operational need or business case for big “baseload” thermal plants—costly, inflexible, now superfluous for reliability—though inflexible mindsets retire even more slowly.

Many in Washington mouth the mushy mantra that climate urgency demands “all of the above.” Actually, no: the more urgent climate change is, the more we must invest judiciously, not indiscriminately, to buy cheap, fast, sure options instead of costly, slow, speculative ones. Only this strategy saves the most carbon per dollar and per year. Anything else worsens climate change.

So the next time you hear some official, eager to appease every constituency, say we support “all of the above—we’re not picking and backing winners,” remember the retort by the dean of U.S. utility regulators, Peter Bradford: “No, we’re not picking and backing winners. They don’t need it. We’re picking and backing losers.”

Amory B. Lovins is an adjunct professor of civil and environmental engineering at Stanford University. He has advised major firms and governments in over 70 countries for 49 years.

No comments yet.

1 This month.

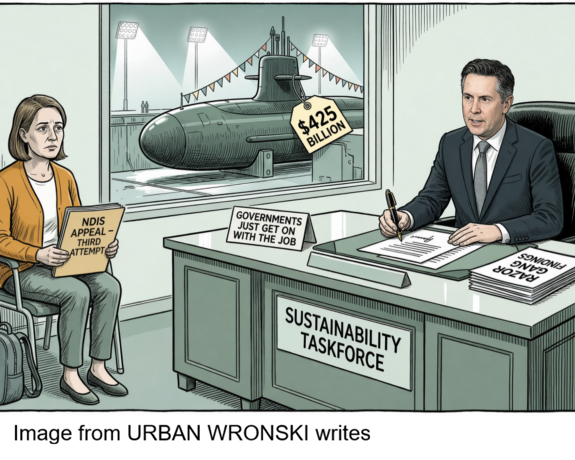

Australians deserve the truth

about

AUKUS – https://aukuspublicinquiry.com/

Australians deserve the truth

about AUKUS

PETITION – To: Prime Minister Anthony Albanese and the Australian Labor Government

of the week – Australians for War Powers Reform (AWPR)

To see nuclear-related stories in greater depth and intensity

Leave a comment